Before plunging into the world of options contracts, every trader and investor should have a strong understanding of option premiums because it is a crucial part of options trading that may significantly impact their profitability.

In this article, we will provide an in-depth exploration of the fascinating world of option pricing, and delve into the four primary factors that have a profound impact on the fluctuation of option premiums.

What is Option Premium?

Option premium is a crucial factor in options trading as it represents the cost of purchasing an option contract, or, more specifically, the cost of obtaining the right to buy or sell an underlying asset at a specified price and within a specific time frame.

Option trading may seem intimidating at first, but with a basic understanding of the factors that affect option premiums, you can begin to develop a trading strategy that works for you.

Key Factors Affect Option Premium

- Underlying asset price

The price of the underlying asset is the most important factor that affects the option premium.

If the underlying asset price increases, the call option premium will also increase, and the put option premium will decrease. On the other hand, if the underlying asset price decreases, the call option premium will decrease, and the put option premium will increase.

- Moneyness:

Moneyness refers to the relationship between the strike price of the option and the current price of the underlying asset.

There are three types of moneyness: in-the-money (ITM), at-the-money (ATM), and out-of-the-money (OTM).

The following figure illustrates the different scenarios for call and put options at different moneyness levels:

Figure 1: Option Moneyness – DBOE Guide to Options Trading

Example of Moneyness:

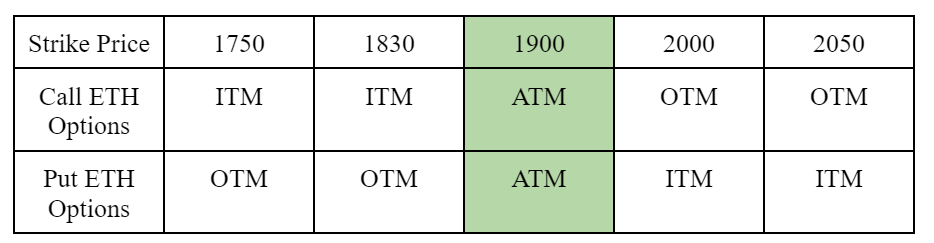

Suppose that the current price of ETH Options is roughly $1900. The following table shows the moneyness of call and put options at different strike prices:

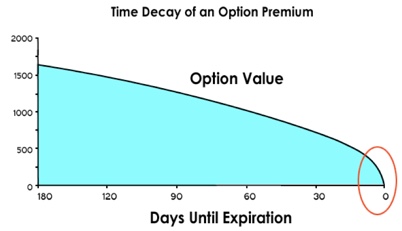

- Time Decay:

Time decay, also known as theta decay, is the reduction in the value of an option as the time to the expiration date approaches. This is because the time value of an option is based on the amount of time left until expiration.

As the expiration date gets closer, the time value of the option decreases, which causes the option premium to decrease.

Figure 2: How Time Decay Affect Options Premium – DBOE Guide to Options Trading

The time value of an option is the portion of the option premium that is based on the amount of time left until expiration. This is because the longer an option has until expiration, the more time there is for the underlying asset to move in the direction that benefits the option holder.

It is important for investors to consider the time value of an option when making trading decisions, as it can have a significant impact on the potential profitability of the trade.

- Implied volatility:

Implied volatility is a critical factor that affects options premiums in the cryptocurrency market, specifically for ETH options. Implied volatility represents the market’s expectation of the volatility of the underlying asset’s price. When there is high uncertainty or expectations of significant price movements, implied volatility increases, and vice versa.

For example, if the market expects ETH’s price to experience high volatility due to upcoming events like network upgrades or regulatory changes, implied volatility will increase. As a result, the premiums for ETH options will also increase since options traders are willing to pay a higher price to hedge against potential losses or capture potential profits.

On the other hand, if there is low uncertainty or expectations of limited price movements, implied volatility will decrease. As a result, the premiums for ETH options will also decrease, making them less expensive.

It’s essential to note that different strike prices and expiration dates have varying sensitivities to implied volatility changes. Short-dated options, for instance, are less sensitive to implied volatility changes than long-dated options since long-dated options have more time value priced into them. Additionally, options with strike prices near the money are more sensitive to implied volatility changes than those that are further in or out of the money.